Tips for affording private school fees

Contents

The five golden rules for affording private school fees

Choosing government or private schooling is a very personal and individual decision with both offering amazing opportunities. But the fact is that a private school education requires a far greater financial commitment. So here’s five golden rules we’ve put together to consider when planning for private school fees.

Rule 1: Set goals and a realistic plan.

Look forward to school fees.

OK, now that we’ve got your attention, what do we mean by looking forward?

Well, you’ve done your research and decided that private school is the way to go. Brilliant. Having made this choice, you want your family to fully embrace and enjoy this stage of your lives; not be burdened by the costs.

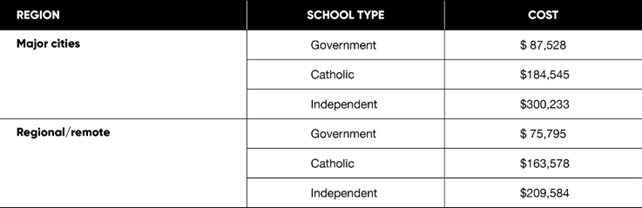

According to the Futurity Investment Group, if your child started in an independent private school in one of Australia’s major cities in 2023, the total estimated cost of education over 13 years of schooling would be $300,000.

And that’s for one child.

Here’s the breakdown of the 13-year schooling costs comparing independent private schools, catholic private schools, and government schools.

Source: Futurity Investment Group Cost of Education Index 2023

These figures factor in the total costs of school fees and levies, extracurricular activities, school uniform costs, books and stationery, travel and computer equipment, including the internet.

To some these costs may not be daunting. For others it’s another story. What is clear is you need to factor in significant education savings into your future, regardless of where you live or if you’ve chosen a private or government school for your child.

You owe it to yourself and your family to set some clear goals. Goals that are based on what you want your overall lifestyle to look like, allowing for the private school fees as well as everyday expenses, mortgage, investments, holidays and other needs. Yes, you may have to make sacrifices along the way, but you want these to be planned and not unexpected.

And above all you want to make the most of this time with your kids.

We can help you with this goal setting exercise. It’s exactly why we created our 10/3/now process. By looking at the short-term (now), medium-term (3 years) and long-term (10 years), you can plan for those big life events and move forward with a sense of security and confidence.

And freedom.

Rule 2: Start your savings early.

One of the golden rules in investing is the earlier you start, the better off you will be. Considering school fees will be one of the major costs your family will face, you can save yourself a lot of heartache (as well as free up your choices) by creating a savings plan as early as possible.

There’s many ways you can do this:

- Set up a specific education savings account for your child as soon as they are born – and make it automated. The best way to do this is to open a dedicated account (such as a savings or term deposit) where every week, fortnight or month an amount is automatically transferred from your main income account. In this way you’ll build up a significant fee fund without even thinking about it. You’ll be amazed how small, regular amounts can add up over time to help cover your future education fees. Creating a structure is the best way to creating freedom.

- Set up a home loan offset account and place your education savings in there, so as this amount increases you’ll also help your mortgage decrease. Top it up with any tax refunds, share dividends and work bonuses. Maybe you could also look at a side hustle (online business, consulting, etc) that could also contribute to these savings. The important thing is to make any income you receive work for you (in other words stay disciplined and focused so you don’t fritter it away).

- Talk to your financial advisor regarding low risk, secure investment opportunities such as managed funds that can help maximise your educational savings.

- If you’re planning to start your child’s private school education from Grade 5 or later, use those early years of primary school to make a sizeable dent in your savings. Factor in the fees you would be paying if your child started private school from prep, and put a good proportion of the difference in a savings account. This is not just a great way to save, it can also prepare you for how you may need to adjust your lifestyle and budget for when your child moves into private school.

- Even before your child commences their schooling there’s fees you need to consider. Private schools typically require a non-refundable application fee that can amount to thousands of dollars. So if you’re applying for more than one school you need to factor in these potential costs into your savings.

Rule 3: Create more savings with a cashflow structure.

Planning for private school fees is one thing. Sticking to the plan is another. The biggest challenge (and opportunity) to stay on track is cashflow.

Unexpected events like we’ve experienced in recent years highlight how important it is to have a strong hold on cashflow, knowing where to set your limits and how to manage your spending.

We’ve all experienced the impact high inflation can have on our mortgages and everyday costs. It’s important to understand that education is one of the segments most vulnerable to inflation, with school fee inflation running at around 7% which will continue to see fee increases over future years.

Factoring in these types of scenarios into your calculations and budgets can go a long way to providing peace of mind in keeping you on track to saving for the education of your child or children.

Again, we can help you here and establish easy to implement strategies and habits so that you control your cashflow, rather than your cashflow controlling you.

Strategies like clearly separating your income into two streams; one to cover fixed spending (education fees, home loan, bills, etc) and one for discretionary (gifts, entertainment, etc) with realistic limits. Balanced with strategies for paying off debt and saving for the future.

We know it’s not easy. Keeping a healthy cashflow takes a huge amount of effort and commitment. But the payoff really comes in allowing you the freedom to choose the education that best meets your child’s needs.

Rule 4: Savings may just be one way.

A savings framework is certainly a great way to allow for education fees. But it may not be the only way.

Discounts

The majority of schools offer a sibling discount, which can be a highly effective way of offsetting some of the costs. Of course, every child is different and being at different schools may be best for their education, but if that’s not a factor then keeping the children at the one school can be a significant cost saver.

Schools also offer discounts for paying fees upfront, but this should only be considered if this aligns with your cashflow structure and savings goals.

Scholarships

All schools offer various types of scholarship programs, so it can be well worth exploring this opportunity for your child. Scholarships can cover either the full or part proportion of the fees.

Grandparents

With the escalating costs of living and education, we’re seeing more and more grandparents wanting to help out with schooling costs. In fact some estimates suggest that at least 60% of private school students have their fees at least partly paid by grandparents.

While this is an amazing gesture, it’s vital that any form of contribution by grandparents is handled with open communication, professional advice and very clear parameters to protect the finances and relationships of all involved.

One of the key considerations is ensuring any payments do not have adverse taxation or pension impacts. For example, the Department of Human Services gifting rule currently allows for a gift up to $10,000 in one financial year and a maximum of $30,000 over five financial years without pension entitlements being affected. There are also different implications depending on whether the contribution is set up as a ‘gift’ or a ‘loan’. Grandparents may also want to explore providing for education through their Will.

With all these factors to take into account, it’s really critical to seek the advice of a trusted advisor – whether that’s a financial expert, lawyer, accountant or all three – to create a framework that meets everyone’s needs and expectations.

Rule 5: Get advice to make smart choices.

A word of caution. What appears the easiest way to paying school fees – school savings schemes, bonds, credit cards – may leave you with a larger debt and limited cashflow.

And less choices.

It’s OK to be worried and cautious about taking on private school fees, especially if you have multiple children to consider. It’s actually a good thing. It shows that you do have your eyes open, and care about your family’s future.

You want to be able to live your Good Life by creating a financial framework that allows you to meet those essential education fees while still being able to enjoy important lifestyle choices like family holidays, sports and other interests.

So our advice is to get as much advice as you can when planning for education costs, especially fees from for private schools. A well thought out savings strategy (not reliant on quick-fixes) can make your child’s private education not only achievable, but financially stress-free.

It’s hard to put a value on that.

If you would like to discuss a plan for your child’s education fees or any other financial advice, our Tribeca Tribe is here for you.